Introduction

For decades, private equity (PE) has been the domain of the ultra-wealthy, institutional investors, and high-net-worth individuals. Think of it as the exclusive club where billionaires and pension funds mingle, investing in privately held companies with the potential for outsized returns. But for the average American saving for retirement through a 401(k) plan, this asset class was largely off-limits—until recently. As of 2025, seismic shifts in regulations, driven by executive actions and evolving fiduciary guidelines, have begun to democratize access to private equity. This guide aims to demystify private equity for 401(k) investors, explaining how it can potentially enhance your retirement portfolio while emphasizing the importance of safety and due diligence.

Why does this matter now? On August 7, 2025, President Donald Trump signed an Executive Order titled “Democratizing Access to Alternative Assets for 401(k) Investors,” which directed the Department of Labor (DOL) to expand opportunities for retirement savers to include alternatives like private equity in their plans. This move builds on earlier efforts, such as the 2020 DOL information letter that cautiously opened the door, but the 2025 order accelerates the process by rescinding prior cautions and encouraging fiduciaries to consider these assets. With over $12.5 trillion in 401(k) assets as of mid-2025, the potential influx of capital into private markets could transform retirement investing.

But let’s be clear: Private equity isn’t a magic bullet. It’s an alternative investment that promises higher returns but comes with unique risks like illiquidity and higher fees. This guide will walk you through the basics—what private equity is, why it was inaccessible, the benefits and risks, how to incorporate it safely into your 401(k), real-world examples, and practical steps to get started. By the end, you’ll have a balanced understanding to discuss with your plan administrator or financial advisor.

Retirement planning is about more than just stocks and bonds. Traditional portfolios have served many well, but with longer lifespans and volatile markets, diversification into alternatives could mean the difference between a comfortable retirement and one filled with financial stress. Studies suggest that adding private equity to a diversified portfolio could boost long-term returns by 2-3% annually, potentially increasing your nest egg by 11-17% over a career. However, this isn’t financial advice—always consult professionals and consider your risk tolerance.

In the pages ahead, we’ll explore how this once-elite asset class is becoming a viable option for everyday investors. Whether you’re a millennial just starting your 401(k) or a boomer eyeing retirement, understanding private equity could unlock new paths to financial security. Let’s dive in.

What is Private Equity?

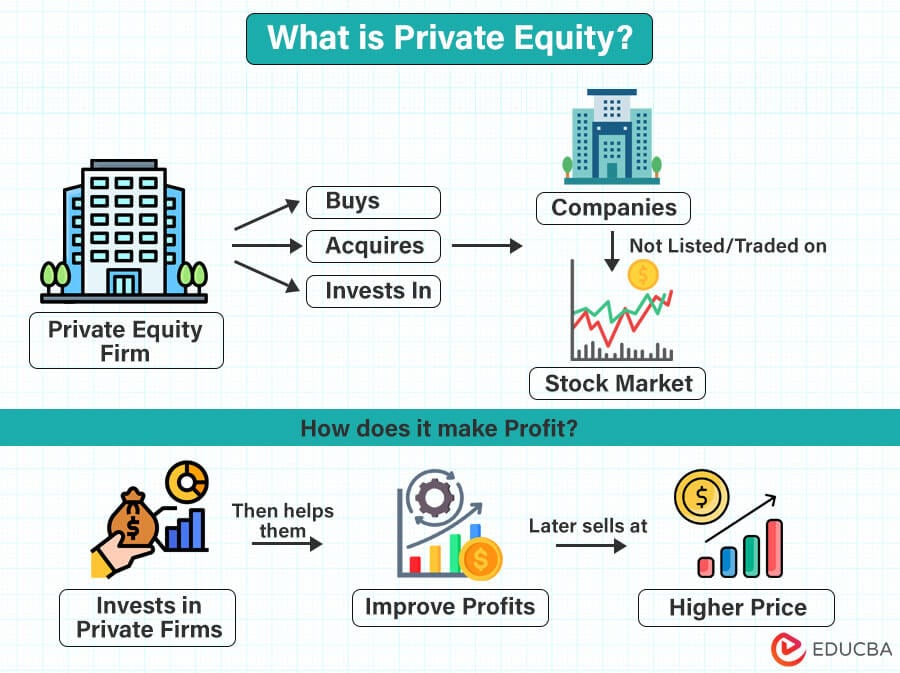

Private equity refers to investments in companies that are not publicly traded on stock exchanges. Unlike buying shares of Apple or Google, which you can do instantly through your brokerage app, private equity involves pooling capital to acquire, improve, and eventually sell private businesses. This asset class is managed by specialized firms like Blackstone, KKR, or Carlyle Group, which raise funds from investors to execute these strategies.

At its core, private equity operates through funds—typically limited partnerships—where investors commit capital for a set period, often 7-10 years. The fund managers (general partners) use this money to buy controlling stakes in companies, ranging from startups (venture capital, a subset of PE) to mature businesses in need of turnaround. They might streamline operations, expand markets, or merge with competitors to increase value. Once optimized, the company is sold—via IPO, to another firm, or strategically—and profits are distributed to investors after fees.

There are several types of private equity strategies:

- Buyouts: The most common, involving acquiring established companies, often with leverage (debt). Leveraged buyouts (LBOs) amplify returns but also risks.

- Venture Capital: Early-stage investments in high-growth startups, like tech firms. Higher risk, higher potential reward.

- Growth Equity: Investing in expanding companies that need capital but aren’t ready for buyouts.

- Distressed Assets: Buying struggling companies at a discount and turning them around.

- Mezzanine Financing: Hybrid debt-equity investments providing capital between senior debt and equity.

What sets private equity apart from public markets? Liquidity—or lack thereof. Public stocks can be sold in seconds; PE investments are “locked up” for years, with limited secondary markets. Valuations aren’t daily; they’re periodic, based on appraisals, which can lead to smoother reported returns but less transparency.

Historically, PE has outperformed public equities. Over the past 20 years, private equity net returns averaged 14.3%, compared to 8.1% for the MSCI World Index. This premium comes from active management: PE firms don’t just invest; they intervene, replacing management, cutting costs, or pivoting strategies. However, this illiquidity premium requires patience—ideal for long-term horizons like retirement.

Fees are another hallmark. Typical structures include a 2% management fee on committed capital and 20% performance fee (carried interest) on profits above a hurdle rate, often 8%. This “2-and-20” model can erode returns if the fund underperforms.

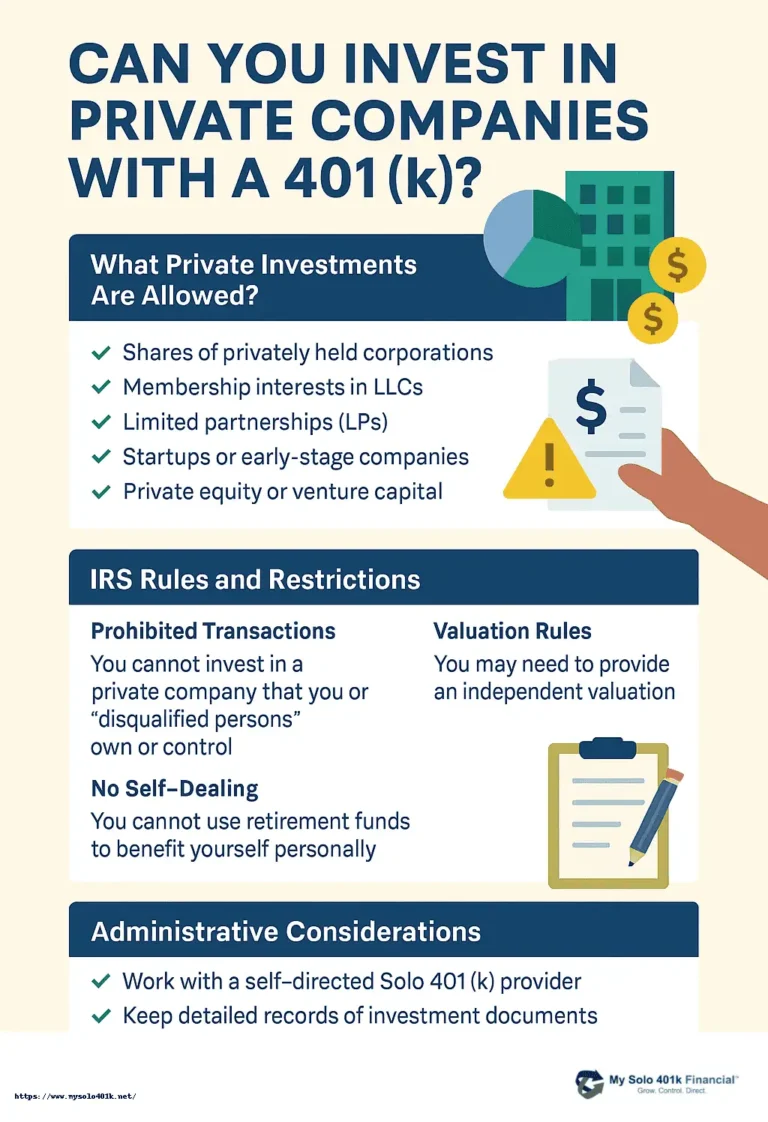

For 401(k) investors, private equity isn’t direct ownership. Instead, it’s accessed via “fund-of-funds” or target date funds (TDFs) that allocate a small portion (5-15%) to PE. This dilutes risks while providing exposure. For example, a TDF might hold 80% stocks/bonds and 10% alternatives, including PE.

Why consider PE now? Public markets are increasingly efficient, with information symmetry reducing alpha (excess returns). Private markets, with less competition, offer untapped opportunities. But it’s not for everyone—suitability depends on your plan’s offerings and personal circumstances.

In essence, private equity is about owning pieces of real businesses, not ticker symbols. It’s capitalism in its raw form: identifying value, adding expertise, and realizing gains. For retirement savers, it represents a shift from passive indexing to a more dynamic approach, potentially yielding better outcomes if managed wisely.

Historical Inaccessibility and Recent Changes

Private equity’s roots trace back to the 1940s, but it exploded in the 1980s with iconic LBOs like RJR Nabisco. For much of its history, PE was reserved for “accredited investors”—those with $1 million net worth or $200,000 annual income—due to SEC regulations under the Investment Company Act of 1940. This exclusivity stemmed from risks: high minimums (often $5-10 million), illiquidity, and complexity deemed unsuitable for retail investors.

In retirement plans, barriers were even higher. ERISA (Employee Retirement Income Security Act of 1974) mandates fiduciary duties, requiring plan sponsors to act prudently. The DOL historically viewed PE as inappropriate for 401(k)s, citing illiquidity conflicting with daily valuations and withdrawals. Pension funds (defined benefit plans) could invest in PE, but 401(k)s—individual accounts—were limited to liquid assets like mutual funds.

Cracks appeared in the 2010s. The JOBS Act (2012) eased crowdfunding, but PE remained elite. By 2020, amid low interest rates and market volatility post-COVID, the Trump administration issued a DOL letter allowing PE in 401(k)s via diversified funds, not direct investments. This was cautious: only as a component of TDFs or balanced funds, with strict fiduciary oversight.

The real game-changer came in 2025. Facing economic pressures—inflation, aging demographics, and underfunded retirements—President Trump signed Executive Order 14330 on August 7, 2025. This order directed the DOL to propose rules clarifying fiduciary duties for alternatives, rescind prior guidance cautioning against PE, and promote access to boost retirement security. It explicitly includes private equity, venture capital, real estate, and even crypto in some forms.

Congressman Kevin Downing introduced supporting legislation, emphasizing democratization. By October 2025, the DOL had pulled old warnings, paving the way for more plans to adopt PE options. Adoption is growing: In November 2024, only 2.4% of sponsors offered PE, but projections for 2025 suggest 10-15% uptake.

These changes address structural hurdles. New vehicles like interval funds or evergreen structures provide semi-liquidity, allowing quarterly redemptions. Technology aids valuations, with AI-driven appraisals reducing opacity.

Yet, challenges remain. Fiduciaries must vet offerings rigorously, ensuring fees justify returns and liquidity meets plan needs. Critics argue this exposes savers to Wall Street’s greed, but proponents see it as empowering workers.

This evolution reflects broader trends: With Social Security strained and pensions rare, 401(k)s must evolve. Private equity’s inclusion could bridge the retirement gap, but only if implemented thoughtfully.

Benefits of Private Equity in 401(k)s

Incorporating private equity into your 401(k) can offer compelling advantages, particularly for long-term savers. The primary allure is the potential for superior returns. Over extended periods, PE has historically outpaced public markets by 3-6% annually, net of fees. For a 401(k) investor, this could translate to hundreds of thousands more in retirement savings. For instance, a 5% allocation to PE in a $500,000 portfolio might add $50,000-$100,000 over 10 years, assuming historical premiums hold.

Diversification is another key benefit. Traditional 401(k)s are heavy on stocks and bonds, correlated to market swings. PE invests in private companies across sectors like healthcare, tech, and consumer goods, often uncorrelated with public indices. During the 2022 market downturn, many PE funds held steady due to long-term holdings, providing a buffer. Vanguard research suggests adding 10-20% alternatives can reduce portfolio volatility by 10-15% without sacrificing returns.

For retirement income, PE’s illiquidity aligns perfectly with 401(k) horizons. You can’t touch funds until 59½ anyway, so locking up a portion for 7-10 years isn’t a drawback—it’s an advantage, forcing discipline. Upon exit, PE often delivers lump-sum gains, ideal for annuitizing or drawing income.

Tax efficiency is underrated. In a 401(k), gains are tax-deferred, amplifying compounding. PE’s structure—fewer distributions until sale—minimizes annual taxes compared to dividend-heavy stocks.

Innovation access is exciting. PE funds back cutting-edge companies, from AI startups to biotech. Everyday investors get indirect exposure to tomorrow’s giants, like early backers of Uber or Airbnb.

Fiduciary-vetted options ensure safety. Plan sponsors must select prudent funds, often with liquidity features. BlackRock’s LifePath funds, for example, include PE sleeves with daily pricing approximations.

Critically, PE can combat inflation. Private companies can adjust prices faster than publics, preserving value in rising-cost environments.

Overall, for patient investors, PE boosts income potential safely within diversified frameworks.

Risks and How to Mitigate Them

No investment is risk-free, and private equity amplifies certain dangers. Illiquidity tops the list: Funds tie up capital for years, with penalties for early withdrawal. In emergencies, this could force sales at a loss.

High fees erode returns—2% management plus 20% carry can consume 30-50% of profits if underperforming. Opacity is an issue: Valuations are subjective, potentially inflating reported performance.

Volatility and leverage add risk. PE uses debt, magnifying losses in downturns. The 2008 crisis saw some funds drop 50%.

Mitigation starts with allocation: Limit to 5-15% of portfolio. Choose diversified funds-of-funds. Demand transparency from sponsors. Monitor fiduciary compliance.

Diversify across PE strategies and vintages. Use interval funds for liquidity.

Ultimately, education and advice mitigate risks, turning PE into a safe booster.

How to Safely Invest in PE via 401(k)

Start by checking your plan: Ask HR if PE options exist, like in TDFs. If not, advocate for addition.

Select vehicles: Opt for TDFs with PE from providers like Fidelity or Vanguard.

Assess fees, track record, liquidity.

Rebalance annually, consult advisors.

Case Studies and Examples

Blackstone’s offerings in 401(k)s show 12% returns.

Conclusion

Private equity offers promise for 401(k) growth, but with caution.

Disclaimer

This is not financial advice. Consult professionals. Investments involve risk.