3rd in a 4-part Series:

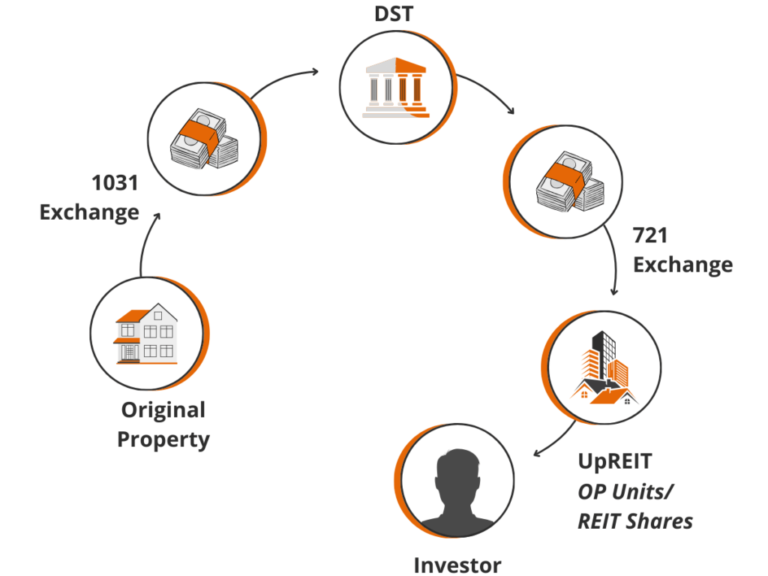

What really adds sizzle to the DST 1031 exchange strategy is another, almost unknown tax code “loophole” of sorts known as the 721 Exchange, or UPREIT. Combined with a DST 1031 exchange, an UPREIT allows the investor to defer capital gains taxes indefinitely, and ultimately eliminate them at death when inherited by an heir or irrevocable, grantor trust that takes a stepped-up basis on the value of of the asset upon its sale.

Capital gains taxes will then be calculated based on the difference between the value of the asset at the original owner’s death and the value of the asset at the time it is sold by the heirs or irrevocable trust.

Accordingly, the less the amount of time between the original owner’s death and the eventual sale of the property (assuming the property appreciates), the less the amount of capital gains tax liability.

A. What is a 721 Exchange (UPREIT)?

A 721 Exchange, also known as an UPREIT (Umbrella Partnership Real Estate Investment Trust) Exchange, is a tax-deferral strategy in real estate where a property owner contributes their real estate into a partnership, typically a real estate investment trust (REIT), in exchange for operating partnership (OP) units.

This allows the property owner to defer capital gains taxes that would otherwise arise from selling the property.

B. Key Features of a 721 exchange:

Tax Deferral: Like a 1031 exchange, the 711 exchange allows deferral of capital gains taxes. However, instead of swapping one property for another, the owner contributes the property to a REIT and receives OP units.

Liquidity and Diversification: The OP units can later be converted into shares of the publicly traded REIT (if applicable), or cash, providing liquidity, though this then becomes a taxable event. Additionally, the owner gains access to a diversified real estate portfolio managed by the REIT.

No Need for Like-kind Property: Unlike a 1031 exchange, there is no requirement for the contributed property to be “like-kind.” The real estate simply has to meet the REIT’s acquisition criteria.

Estate Planning Benefits: OP units can be passed to heirs with a step-up in basis, potentially reducing estate taxes.

C. 721 Exchange Process:

Contributing Property: The property owner transfers their property to the REIT’s operating partnership.

Receiving OP Units: In return, the owner receives partnership units in the REIT, equivalent in value to the property contributed.

Tax Deferral: The capital gains tax on the appreciation of the property is deferred until the OP units are sold or converted to REIT shares.

Future Conversion: If the REIT is publicly traded, OP units may be converted to publicly-traded shares, providing liquidity, though this then becomes a taxable event.

D. Limitations and Considerations:

Not Reversible: Once the property is contributed, it is owned by the REIT, and the process cannot be undone.

Loss of Direct Control: The property owner loses control over the specific real estate asset.

Qualified REIT: The REIT must be structured to accept proeprty contributions and issue OP units.

Tax Implications upon conversion: Converting OP units into REIT shares or cash is a taxable event.

E. A 721 Exchange is Ideal for Property Owners Seeking:

- To defer capital gains taxes without identifying a new, “like-kind” property.

- A more passive investment approach.

- Access to diversified and professionally managed real estate portfolios.

- Enhanced liquidity options for their real estate investment.

Eventually, a DST will end

(most have a pre-determined lifespan of 5-10 years), at which time the investor’s options are to either 1031 into another DST, or ideally, to be bought by a REIT fund that wants to own and operate these buildings long-term.

Using a 721 exchange, the investor can roll into the REIT fund, again deferring capital gains taxes. At the end of this process, the investor would own shares in a private or public REIT without causing a taxable event, and which could then be fractionally liquidated by the investor with the click of a mouse. The investor could sell any fraction of his investment and pay the capital gains tax only on that amount.

Finally, if the REIT is then held to the owner’s death, the REIT’s heirs can then take a stepped-up basis, essentially eliminating capital gains taxes if the property is sold at the time of the owner’s death and not held long enough to appreciate. Or, if inherited by an irrevocable, grantor trust, the trust can take the stepped-up basis.

This is how an investor can sell a high-value real estate asset and defer the capital gains tax liability almost indefinitely while alive, and eliminate it entirely upon death!

Now that you have learned the basics of combing a Delaware Statutory Trust (DST) 1031 exchange with a 721 exchange of investment real estate and its advantages, let’s move on to the fourth and last article in our 4-part series, “Taking a Stepped-up basis on an UPREIT Asset.”

Disclosure: For educational purposes only. Not legal or tax advice. Consult your professional advisor/s before taking any action regarding this subject.