4th in a 4-part Series:

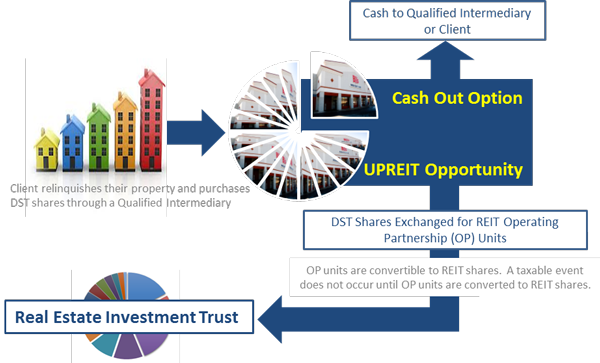

When an individual heir or an irrevocable grantor trust inherits an interest in an UPREIT (Umbrella Partnership Real Estate Investment Trust), the possibility of receiving a stepped-up basis depends on the specific structure of the inherited asset and the applicable tax laws.

A. Direct Ownership of REIT Shares:

If the inheritance involves direct ownership of publicly-traded or private REIT shares, the heir or trust does not receive a stepped-up basis for the underlying properties properties held by the REIT. This is because the REIT is a separate entity that owns the properties, and the stepped-up basis applies only to the securities (the REIT shares) themselves.

B. Ownership of OP (Operating Partnership) Units:

If the inheritance involves Operating Partnership (OP) units in an UPREIT structure:

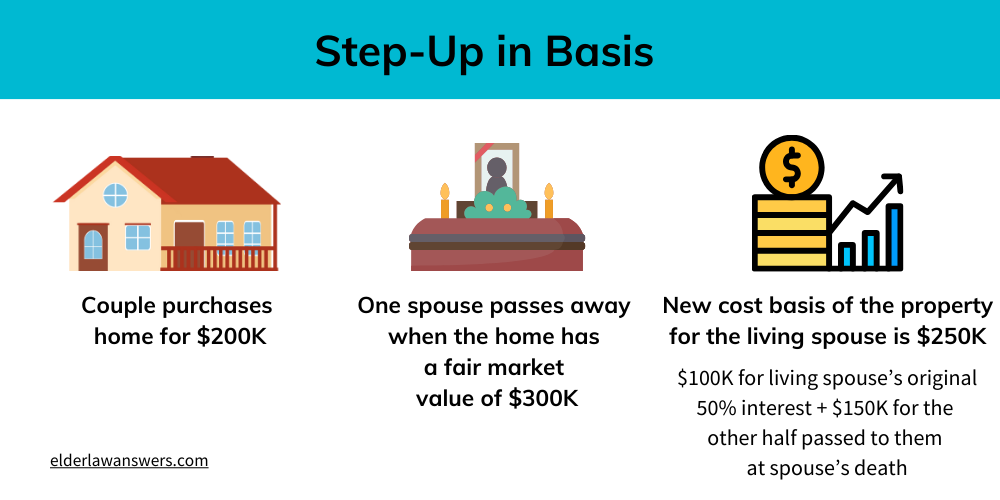

1. Stepped-up Basis on Death: Generally, OP units are treated as partnership interests. When inherited, they typically receive a stepped-up basis to the fair market value at the decedent’s death, in accordance with Internal Revenue Code 1014.

2. Effect on Taxation: This step-up can reduce future capital gains tax liabilities if the heir later converts the OP units into REIT shares or liquidates them.

C. Irrevocable Grantor Trusts:

1. If the trust is considered a “grantor trust” for tax purposes, the decedent is treated as the owner of the trust’s assets. The trust’s assets, including OP units or REIT shares, would be included in the decedent’s estate, and could receive a stepped-up basis upon the decedent’s death.

2. If the irrevocable trust is not a grantor trust (e.g. a non-grantor, irrevocable trust), the assets held in the trust do not receive a stepped-up basis upon the death of the trust’s grantor, as the assets are not included in the grantor’s estate.

D. Estate Tax Considerations:

Again, whether a stepped-up basis is granted depends on whether the inherited assets are included in the decedent’s taxable estate for estate tax purposes. If included, they are eligible for a stepped-up basis.

E. Key Points to Confirm:

1. Nature of the Ownership: Confirm whether the inheritance involves REIT shares, OP units, or other structures.

2. Estate Planning Documents: Review the decedent’s estate plan and the type of trust to determine eligibility for a stepped-up basis.

3. Professional Advice: Tax Rules can be complex, and consulting with a tax advisor or estate planning attorney is critical for precise application to individual circumstances.

Here’s a specific scenario to illustrate how a stepped-up basis might work when inheriting an UPREIT interest:

Scenario: Inheriting OP units via an irrevocable, grantor trust.

Background:

1. Decedent’s Ownership:

a. Jane owns 10,000 Operating Partnership (OP) units in an UPREIT structure. These units are held within an irrevocable grantor trust, and Jane is treated as the owner of the trust for income tax purposes.

b. The OP units were originally acquired by Jane for $1,000,000 (basis), and are now worth $5,000,000 at the time of her death.

2. UPREIT Structure:

a. The OP units can be converted into REIT shares on a 1:1 basis or liquidated for cash, although this then becomes a taxable event.

3. Heir:

The irrevocable grantor trust passes the OP units to Jane’s son, Mike, upon her death.

Tax Implications:

1. Step-up in basis:

a. Since the trust is a grantor trust, the assets within the trust are included in Jane’s taxable estate. Upon her death, the OP units receive a step-up basis to their fair market value of $5,000,000 under IRC 1014.

2. Future Tax Benefits:

a. Mike inherits the OP units with a new basis of $5,000,000.

b. If Mike converts the units to REIT shares or sells them, his taxable capital gain will be calculated based on the stepped-up basis.

c. If he sells immediately for $5,000,000, there is no taxable gain.

d. If he holds, and the value increases to %6,000,000, his taxable gain will only be $1,000,000 ($6,000,000 sale price – $5,000,000 stepped-up basis).

3. Estate Tax:

The $5,000,000 value of the OP units is included in Jane’s estate for estate tax purposes. If her estate exceeds the federal estate tax exemption, it may be subject to estate taxes.

N.B. As of December 2024, the federal estate and gift tax exemption is $13.61 million per individual. For married couples, the combined exemption is $27.22 million. This allows significant tax-free transfers of wealth during life or at death. These thresholds are the highest they’ve ever been but are set to “sunset” at the end of 2025, reverting to approximately $7 million per individual unless Congress acts to extend or amend the current law

4. Income Tax on UPREIT Conversion:

If Mike converts the OP units into REIT shares, this is a non-taxable event because of the stepped-up basis. The new REIT shares would retain the stepped-up basis of $5,000,000..

Alternative Scenario:

If Jane’s trust was an irrevocable non-grantor trust, the OP units would not be included in her taxable estate. In this case:

a. The OP units would not receive a stepped-up basis.

b. Mike would inherit the units with Jane’s original $1,000,000 basis , resulting in a larger taxable gain if he sells or converts the units.

Key Takeaways:

a. A stepped-up basis is a significant tax benefit for inherited assets included in a decedent’s estate.

b. Trust structure (grantor vs. non-grantor) and estate tax planning directly affect whether the stepped-up basis applies.

c. Professional estate planning can help optimize tax outcomes in such scenarios.

Estate Tax Calculations and Planning Strategies for the Given Scenario:

1. Estate Tax Calculation

Facts Recap:

a. Fair Market Value (FMV) of the OP Units = $5,000,000.

b. Jane’s Other Assets: Assume Jane has an additional $10,000,000 in other assets (e.g., cash, real estate, investments).

c. Total Estate Value: $5,000,000 (OP units) + $10,000,000 (other assets) = $15,000,000

d. Federal Estate Tax Exemption: (December 2024) = $13. 61 million per individual.

e. Estate Tax Rate: For 2024, the federal estate tax rate applies progressively to the portion of an estate exceeding the exemption threshold ($13.61 million per individual). The rate starts at 18% for amounts just over the exemption and increases incrementally, reaching a maximum of 40% for amounts exceeding $1 million above the exemption.

Estate Tax Calculation:

a. Taxable Estate: $15,000,000 – $13,610,000 = $1,390,000.

b. Estate Tax Liability: $1,390,000 x 40% = $556,000.

Outcome:

Jane’s estate owes $556,000 in federal estate taxes due to the OP units and other assets exceeding the exemption threshold.

2. Strategies to Reduce Estate Tax

A. Gifting OP Units During Lifetime:

1. Jane could gift portions of her OP units to her son during her lifetime, reducing the taxable estate.

a. Annual Gift Tax Exclusion: For 2024, the Annual Gift Tax Exclusion is $18,000 per recipient, per year. This means that Jane can gift up to $18,000 to any number of recipients in a year without reducing her $13,610,000 lifetime gift and estate tax exemption. For married couples, the exclusion can be combined, allowing up to $36,000 per recipient, per year without triggering gift tax or impacting their $27,220,000 lifetime exemption.

b. Lifetime Gift Exemption: For 2024, Jane can gift up to $13,610,000 without triggering gift taxes.

Important Consideration: Gifting removes the OP units from Jane’s estate, but forfeits the stepped-up basis. Mike would inherit Jane’s original $1,000,000.

B. Setting Up a Grantor Retained Annuity Trust (GRAT):

1. Jane could transfer the OP units into a GRAT, allowing her to:

a. Retain an annuity for a specified period.

b. Transfer the OP units’ remainder interest to Mike with minimal gift tax.

c. Any appreciation in value above a “hurdle rate” escapes estate taxation.

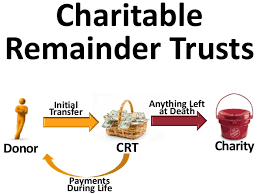

C. Charitable Remainder Trust (CRT):

1. Jane could place the units into a CRT.

a. The trust then provides her with income during her lifetime.

b. Upon Jane’s death, the remaining assets go to charity, removing them from her taxable estate.

c. Potential income tax deduction for the charitable contribution.

D. Leveraging Discounts for Valuation:

Jane owns a minority interest in the UPREIT (OP units), valuation discounts (e.g., for lack of control or marketability), may apply.

A discount of 20-30% could reduce the $5,000,000 FMV to $3,500,000-$4,000,000, lowering her taxable estate.

E. Utilizing the Portability Rule:

If Jane is married, her unused estate tax exemption could be transferred to her spouse under the portability rule. This would effectively double the exemption to $27,220,000 in 2024, thereby eliminating estate taxes.

3. Scenario with Non-grantor Trust:

If Jane had an irrevocable non-grantor trust holding the OP units:

a. The OP units would not be included in her taxable estate.

b. Estate tax liability would be reduced, but the OP units would not receive a stepped-up basis.

c. Mike would inherit the units with Jane’s original $1,000,000 basis, resulting in significant capital gains upon sale or conversion.

4. Blended Strategy for Optimal Results:

a. Use a GRAT or CRT to remove the OP units from Jane’s taxable estate, while retaining income benefits.

b. Gift some OP units annually to Mike, leveraging the annual gift tax exclusion.

c. Retain a portion of the OP units in a grantor trust to ensure stepped-up basis for some assets.

Disclosure: For educational purposes only. Not legal or tax advice. Consult your professional advisor/s before taking action regarding this subject.